Daily Alpha Insights: E-Infrastructure Transmission — STRL Earnings Validation (May 5, 2026)

As of: May 5 close ET | Market Regime: AI-CapEx Driven with Geopolitical Easing

Format: Educational only—not investment advice.

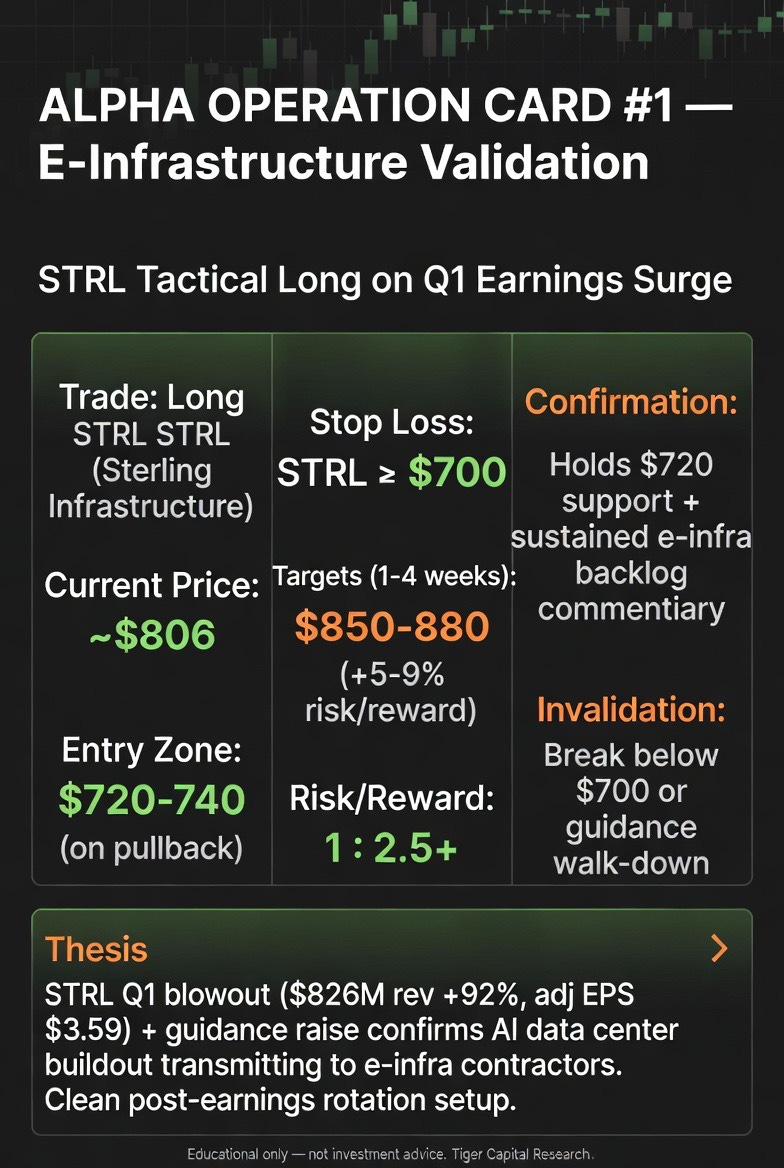

Alpha Operation Card:

Executive Summary

The single most important driver is Sterling Infrastructure’s (STRL) record Q1 results: revenue $825.7M (+92% YoY, massive beat), adjusted EPS $3.59 (+120%), and full-year guidance raised sharply (midpoint now implying ~51% growth). E-Infrastructure Solutions (data center/power work for hyperscalers) drove the bulk. Stock surged +52% to close ~$806. The three most exposed assets are STRL itself, other e-infra contractors, and AI buildout enablers. Consensus still prices infrastructure as lagging/cyclical; the mechanical truth is the backlog, organic growth (>55%), and guidance confirm hyperscaler capex is hitting the ground now—exactly as oil eases on truce optimism.

Market Focus Today: The Mechanics of the Move

First-order effect: STRL reported blowout numbers and raised outlook; the stock gapped up and held the move on volume >4x average.

Second-order effect: E-Infrastructure segment (72% of revenue) showed 23.5% adjusted operating margins and record backlog contribution. This validates that AI data center/power demand is transmitting directly to heavy civil contractors—no longer “future” hype.

Market Pricing: Broader indices rebounded (S&P ~+0.8%, Nasdaq ~+1%) on truce news and oil drop (~3.5%). The surprise transmission is STRL decoupling violently higher, proving the physical layer of AI capex is real and accelerating.

1. The Contrarian Research Questions

• Is this a fundamental re-rating or one-day earnings noise? Record backlog, >55% organic growth, CEC acquisition integration, and aggressive full-year raise point to structural demand, not noise.

• Who is the “forced buyer/seller” at this level? Generalist value/cyclical funds forced buyers chasing the move; AI skeptics or those anchored in pre-earnings levels are the forced sellers.

• Is realized vol matching options pricing? STRL vol exploded cleanly on the earnings reaction while broader VIX compressed—options had not priced the full transmission strength.

2. Desk Judgment & Selection Bias

We are ignoring generic truce headlines and broad Mag7 noise. The evidence is strongest in STRL’s segment-level numbers (E-Infrastructure margins and backlog) and the explicit guidance raise. We are most uncertain on the exact pace of further hyperscaler awards, but the directional validation of AI buildout flowing to contractors is the clearest mechanical edge today.

3. The Alpha Opportunities (The “Core Signal”)

Alpha Opportunity 1: STRL Catch-Up / Hold on Validated AI E-Infrastructure Demand

Setup: STRL closed ~$806 after +52% surge from Friday’s ~$530 area. The move was driven by clean earnings beats and guidance raise; stock held above $700 intraday support on heavy volume.

The Consensus Blindspot: Herd still treats e-infra contractors as old-economy cyclical plays. They miss that hyperscaler data center/power projects (Microsoft, Amazon, etc.) are now the dominant backlog driver and are delivering record margins and visibility.

Why it Matters: This is the mechanical transmission—AI capex is no longer just chips or software; it is flowing to physical contractors with real cash flow and backlog acceleration. Forces rotation into proven execution names as the broader tape digests truce/oil easing.

Evidence & Positioning: 92% revenue growth (organic +55%+), adjusted EBITDA margins >20%, record backlog, and full-year guidance raise all tie directly to e-infrastructure. Positioning had been underweight this sub-sector relative to the now-validated capex reality.

Confirmation Triggers:

• STRL holds $720–740 on any post-surge pullback.

• Continued hyperscaler commentary or follow-on e-infra awards in sector.

• Oil stays below $105 supporting broader risk appetite.

Invalidation Triggers:

• STRL breaks and closes below $700 on heavy volume.

• Any material guidance walk-down or backlog erosion in future prints.

• Broad risk-off that swamps the infrastructure rotation.

Trade Framing: If STRL holds $720–740 support into the back half of the week, the path to $850–880+ opens due to thin seller interest and continued rotation flows. Tactical long STRL on any near-term dip (higher conviction on execution and backlog); size to portfolio risk. This is the cleanest, real-time operational setup right now.

(See Alpha Operation Card below for exact tactical levels.)

(No second alpha today—focus stays tight on this earnings-driven transmission edge.)

Process Hygiene & Risk Evaluation

Odds of over-fitting are low; the numbers (92% growth, 120% EPS beat, guidance raise) and price action are unambiguous. Tomorrow’s data point that kills the thesis: any negative surprise in follow-on industrial or e-infra prints or sharp risk-off derailing the AI capex narrative. Liquidity remains supportive but event-driven around earnings season.

Key Takeaways & The “Next 48 Hours” Watchlist

• Key Level: STRL $720 support.

• Catalyst Timer: Any follow-through e-infra or industrial commentary this week.

• Risk Signal: STRL break below $700 or VIX spike confirming broad de-risking.

Call to Action

Subscribe to Tiger Capital Research for founder-calibrated daily dispatches and exclusive institutional-grade analytics.